Yield Aggregators on Solana: Lulo, Tulip and Beyond

Solana's yield aggregator landscape has changed fast. Lulo routes $86M across lending markets. Tulip is a ghost town. Kamino blurs the line between lender and aggregator. Here's where things stand in May 2026.

The Aggregator Landscape Shifted

A year ago, Solana had a handful of yield aggregators competing for deposits. Today, one is dominant, one is dead, and the definition of "aggregator" itself has gotten blurry.

If you deposited USDC into Tulip Protocol in early 2024, you were using the first yield aggregator built on Solana. If you check Tulip today, the protocol holds less than $5,000 in TVL. Meanwhile, Lulo quietly crossed $100M in deposits before settling around $86M. And Kamino, technically a lending protocol, runs automated strategies that look a lot like aggregation.

This post breaks down where Solana yield aggregators stand right now, what each one actually does with your capital, and which trade-offs you're making with each option.

What Aggregators Do (Quick Version)

If you want the full explainer, we wrote one: What Is a Yield Aggregator?

Short version: you deposit a token (usually USDC). The aggregator's smart contracts scan lending rates across multiple protocols. Your capital gets routed to whichever market pays the most. When rates shift, the aggregator rebalances. You earn yield without manually comparing protocols.

The promise is simple: better rates through automation. The cost is an extra smart contract layer between you and the underlying protocol, which means more trust assumptions and more attack surface.

Lulo: The Leading Pure Aggregator

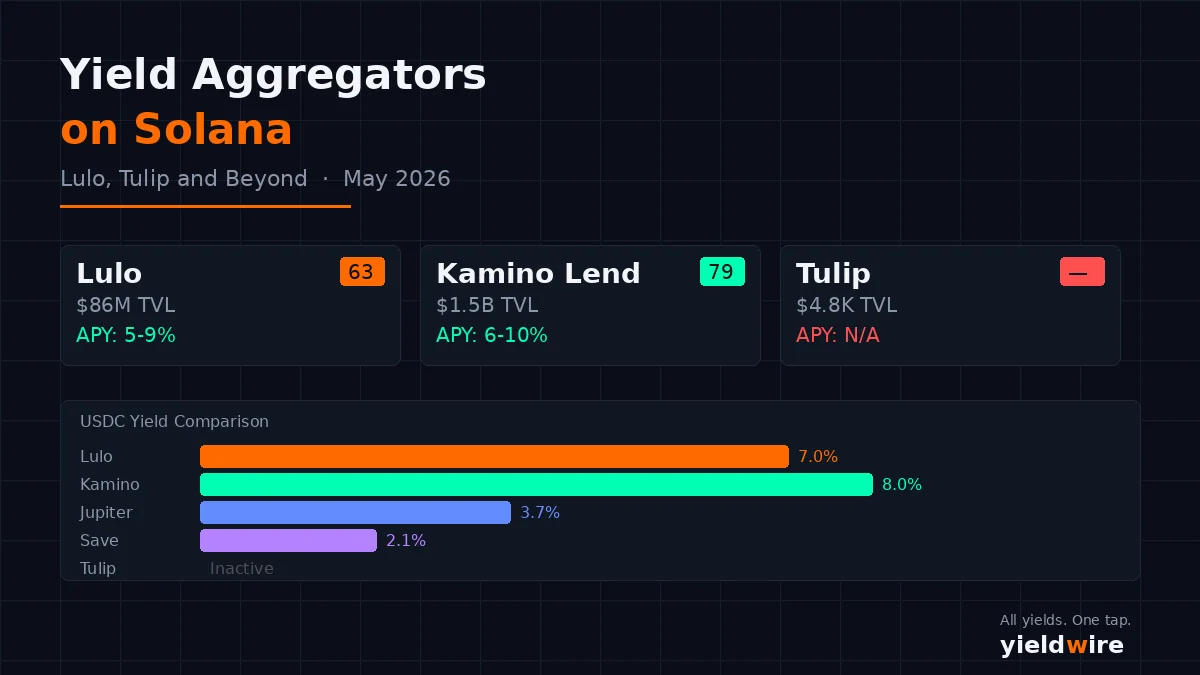

Lulo is the closest thing Solana has to a pure yield aggregator right now. It accepts stablecoin deposits and routes them across multiple lending markets: Kamino, Drift, MarginFi, Save, Maple, and Meteora.

How It Works

You deposit USDC (or USDT). Lulo's routing engine checks which integrated protocol currently offers the highest lending rate. Your capital moves there. When a better rate appears elsewhere, Lulo migrates your position. This happens automatically, with no gas fees on your side.

Lulo offers three modes:

Lulo Protect. Conservative routing. Lower APY (~5%), but stricter rules about which protocols qualify. Think of it as the aggregator with guard rails.

Classic. Standard optimization. Routes to the highest available rate across all integrated venues.

Boosted. More aggressive. Higher potential APY, but routes into higher-risk opportunities.

The Numbers

| Metric | Value |

|---|---|

| TVL | ~$86M (May 2026) |

| Typical USDC APY | 5-9% |

| Peak TVL | $100M+ |

| Integrated protocols | 6 (Kamino, Drift, MarginFi, Save, Maple, Meteora) |

| Fee model | No optimization fees |

| Platform | iOS only (Android planned) |

Lulo's APY for USDC typically sits between 5% and 9%, depending on market conditions. During periods of high borrow demand across Solana, rates can spike higher. During quiet periods, they compress toward the 5% floor.

Risk Profile

Lulo scores 63/100 (Grade C) on yieldwire's security methodology. That's not a red flag, but it's worth understanding why.

The core issue with any aggregator is compounded exposure. When you deposit into Lulo, your capital passes through Lulo's contracts and then into one or more underlying protocols. A bug in either layer can affect your funds. That's two trust assumptions instead of one.

Lulo's TVL is also heavily weighted toward Meteora vaults at times, which creates concentration risk. If the routing engine sends most deposits to a single protocol, you don't get the diversification benefit you might expect.

There's no token yet. Lulo has hinted at a governance token tied to the Protect feature, but nothing confirmed. That means no reward yield component right now... which is actually a plus. The APY you see is base yield, not token incentives.

Tulip Protocol: A Solana Pioneer, Now a Ghost

Tulip (originally SolFarm) was the first yield aggregator on Solana. It launched auto-compounding vaults for LP positions and lending strategies back when the ecosystem was young and full of incentive programs.

The numbers tell the story:

| Metric | Value |

|---|---|

| TVL | ~$4,800 (May 2026) |

| Token (TULIP) market cap | ~$30,000 |

| Status | Effectively inactive |

That's not a typo. Less than $5,000 in total value locked. The TULIP token, which once traded above $50, sits near its all-time low.

What happened? The same thing that happens to most DeFi protocols built primarily on incentive-driven yield: the incentives stopped, the capital left, and the team moved on. Tulip had announced plans for additional vaults, tiered staking, a "yield hopping" product, and a yield-bearing stablecoin. None materialized into products with traction.

Tulip matters as history. It proved the aggregator model could work on Solana's fast, cheap infrastructure. But it's not a place to park capital in 2026.

Kamino: The Line Gets Blurry

Kamino Finance isn't a yield aggregator in the traditional sense. It's a lending protocol with $3.2B in TVL, the largest DeFi application on Solana. But its automated liquidity vaults do something very aggregator-like.

Kamino's lending side (Kamino Lend) works like a standard lending market: deposit USDC, earn interest from borrowers. Current USDC supply rates sit around 6-10%, mostly base yield with some KMNO token incentives on top. Security score: 79/100 (Grade B) on yieldwire.

The aggregator-adjacent part is Kamino Liquidity. These vaults accept LP deposits and automatically manage concentrated liquidity positions on Orca and Raydium. They rebalance ranges, compound fees, and convert LP positions into fungible kTokens you can use elsewhere.

| Kamino Product | Type | USDC APY Range | TVL |

|---|---|---|---|

| Kamino Lend | Lending | 6-10% | ~$1.5B |

| Kamino Liquidity | Automated LP vaults | 8-15% avg | ~$167M |

The difference from a pure aggregator like Lulo: Kamino's lending side IS the underlying protocol. There's no extra routing layer. When you deposit USDC into Kamino Lend, your capital stays in Kamino's contracts. One trust assumption instead of two.

Kamino Liquidity vaults add more complexity. They actively manage LP positions, which means impermanent loss is a real factor. But the automation removes the need to manually rebalance concentrated liquidity ranges, something that's impractical for most users.

For pure stablecoin lending, Kamino Lend is arguably a better option than an aggregator, because you get competitive rates without the additional smart contract layer. The aggregator advantage only kicks in when rates across protocols diverge significantly... and for USDC lending on Solana, the top protocols tend to cluster within a few percentage points of each other.

Other Aggregators Worth Knowing

Francium

Francium combines yield aggregation with leveraged farming. You can deposit assets for standard yields or take leveraged positions for amplified returns. The leverage adds a layer of liquidation risk that pure aggregators don't have. Currently a niche product for experienced DeFi users.

SoraLabs

A newer entrant building a data-driven aggregator with a smart risk engine. Advertises zero optimization fees and real-time reallocation. Still early, with limited TVL data available. Worth watching but not yet established.

Beefy Finance

Multi-chain auto-compounder with some Solana support. Beefy focuses on LP vault compounding rather than lending rate optimization. If you're already using Beefy across Ethereum or other chains, the Solana integration extends that same model.

Comparison: How They Stack Up

| Aggregator | TVL (May 2026) | USDC APY | Security Score | Risk Level | Best For |

|---|---|---|---|---|---|

| Lulo | ~$86M | 5-9% | 63/100 (C) | Medium | Hands-off stablecoin yield |

| Kamino Lend | ~$1.5B | 6-10% | 79/100 (B) | Lower | Direct lending, higher security |

| Kamino Liquidity | ~$167M | 8-15% | 76/100 (B) | Medium | Automated LP management |

| Francium | Small | Variable | N/A | Higher | Leveraged strategies |

| Tulip | ~$4.8K | N/A | N/A | Do not use | Nothing (inactive) |

When an Aggregator Makes Sense

Aggregators aren't automatically better than direct lending. Here's when each approach fits.

Use an aggregator (Lulo) when:

You want stablecoin yield without monitoring rates across six protocols. You're okay with an additional smart contract layer. You value convenience over minimizing trust assumptions. The rate differential between protocols is wide enough to justify the extra risk.

Use direct lending (Kamino, Jupiter Lend) when:

You want fewer trust assumptions. You're depositing enough that a 1-2% rate difference matters less than security. The protocol you're using already offers competitive rates. You want to understand exactly where your capital sits at all times.

Skip aggregators entirely when:

You're earning liquid staking yield (JitoSOL, jupSOL, mSOL). These are single-protocol, base-yield products with no aggregation needed. Current rates: 5.4-6.5%. Security scores: 76-84/100. Compare liquid staking yields →

The Aggregator Risk Checklist

Before depositing into any aggregator:

Check the integrated protocols. Where can the aggregator send your capital? If any of those protocols have poor security or low TVL, your funds could end up there.

Verify withdrawal terms. Can you pull out instantly, or are there queues? During market stress, withdrawal delays can turn a yield strategy into a locked position.

Look at concentration. Is the aggregator spreading capital across venues, or dumping everything into one protocol? Diversification is supposed to be the selling point.

Read the audit history. The aggregator's routing contracts are complex. They need their own audits, separate from the audits of underlying protocols.

Track where your capital actually is. Some aggregators make this transparent. Others don't. If you can't see where your USDC is right now, that's a problem.

We track risk scores for all aggregated pools on yieldwire. Every pool shows its security score, TVL, and APY breakdown (base vs reward). Explore all yields →

Bottom Line

Solana's yield aggregator market is consolidating. Lulo is the main pure aggregator, doing one thing well: routing stablecoins to the highest lending rate. Tulip is history. Kamino is eating the aggregator's lunch by being a top lending protocol that also automates LP management.

For most users depositing stablecoins, the practical choice is between Lulo (higher potential APY, more smart contract risk) and Kamino Lend (slightly lower APY ceiling, stronger security profile, simpler trust model).

The gap between them is narrow enough that your decision should come down to risk tolerance, not yield chasing. A 1-2% APY difference matters a lot less than a smart contract exploit.

Compare all aggregator and lending yields, risk-scored and updated hourly: yieldwire.xyz/yields

Explore all Solana yields · Risk scores · Follow @yieldwirexyz

This article is for informational purposes only. It is not financial advice. Yield rates are variable and past performance does not guarantee future returns.

Track all Solana yields in real time

Compare APYs across lending, LP, and liquid staking protocols on the YieldWire dashboard.

Open Dashboard →