MarginFi on Solana: Current Yields and What Changed After Relaunch

MarginFi was a top-three Solana lender at $811M TVL in 2024. After a leadership blowup, a year of airdrop limbo, and a rebrand to Project 0, it now runs $29M. Here are the live supply yields, the security score, and what the relaunch actually changed.

The Short Version

MarginFi is not called MarginFi anymore. The lending protocol now operates under Project 0, the brand the team launched alongside its long-delayed token. The contracts are the same marginfi-v2 codebase. The deposits are not.

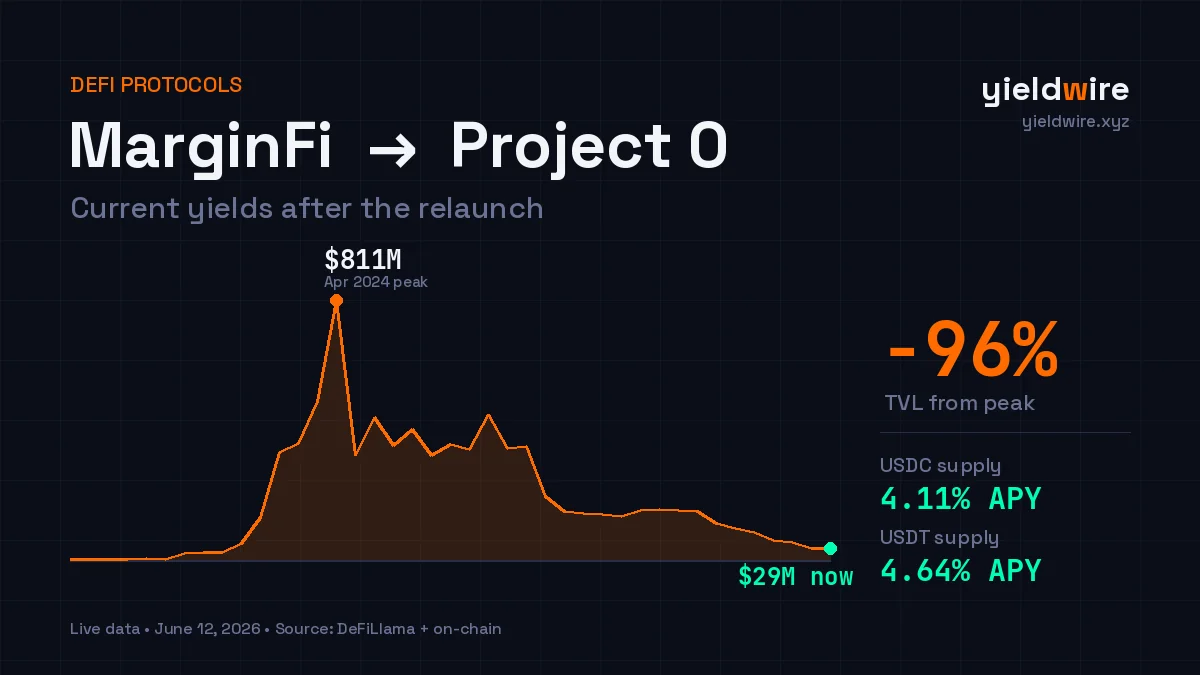

At its 2024 peak, MarginFi held $811M in TVL and ranked among the top three lenders on Solana. Today the lending markets hold about $29M. That is a 96% drawdown from peak, and most of it left before the rebrand, not after.

This post pulls the live supply yields, reads them honestly, and looks at what the relaunch changed and what it did not. If you are weighing a deposit, the yields are competitive on stables and thin everywhere else. The bigger question is whether you want exposure to a protocol that lost almost all of its liquidity and is now rebuilding under a new name.

What Actually Happened

MarginFi's collapse was not a hack. It was a confidence run.

In April 2024 the protocol sat at $811M TVL. That same month its co-founder and CEO Edgar Pavlovsky publicly resigned and started posting critically about the project. Users read the signal and moved. The Block reported roughly $155M in outflows in the days that followed. By May 2024, TVL had fallen to $327M. It never fully recovered.

The other problem was the airdrop. MarginFi ran a points campaign for over a year with no token. Deposits stayed partly because users were farming an allocation that kept slipping. Every quarter the token did not ship, more of that patient capital gave up.

The relaunch is the resolution to both problems. In late 2025 the team rebranded to Project 0, a decentralized prime broker built on top of the existing lending stack. MarginFi points migrated to Project 0 points on a 1:1 basis. Governance discussion opened in October 2025, the token generation event was announced at Breakpoint, and token distribution completed by early December 2025, with 20% of supply going to MarginFi and Project 0 points holders.

So the token finally exists. The leadership question is settled. What did not change is the liquidity. TVL kept bleeding through the transition and now sits near $29M.

What MarginFi Is Now

Strip the branding and the product is two layers.

The base layer is the marginfi-v2 lending protocol. Users supply assets to earn yield, borrowers post collateral and pay interest, and rates float with utilization. A single marginfi account can hold up to 16 assets at once, which is more cross-collateral flexibility than most Solana lenders offer.

The lending markets split three ways. Global markets pool interconnected assets so collateral in one position backs borrows in another. Isolated markets wall off riskier or newer assets with their own parameters, so a long-tail token cannot drag down the main pool. The native stake market lets you post liquid staking tokens as collateral while they keep earning their underlying staking yield.

The layer on top is Project 0 itself, pitched as a prime broker. The idea is cross-venue margining: post your whole Solana DeFi portfolio as collateral and borrow against it across integrated venues, with planned routing into protocols like Kamino. That is the ambition behind the rebrand. For a depositor today, the part that matters is still the lending markets underneath.

Live Supply Yields

These are the current supply APYs on the lending markets, pulled from on-chain data on June 12, 2026. APY here is the base lending rate paid to suppliers. It moves with utilization, so treat these as a snapshot, not a guarantee.

| Asset | Supply APY | Pool TVL | Notes |

|---|---|---|---|

| SOL | 5.39% | ~$450K | Highest base rate, thin pool |

| USDT | 4.64% | ~$361K | Top stablecoin rate |

| PYUSD | 4.12% | ~$60K | Tiny pool, rate-sensitive |

| USDC | 4.11% | ~$1.1M | Deepest stablecoin market |

| USDS | 3.24% | ~$227K | Lower utilization |

| WBTC | 0.31% | ~$842K | Collateral asset, minimal lending demand |

| jitoSOL | 0.16% | ~$5.0M | Largest pool, value is in staking yield |

| mSOL | 0.19% | ~$3.3M | Same logic as jitoSOL |

Total lending TVL across all 51 markets is about $29.9M.

Two things to read carefully.

First, the stablecoin rates are real and competitive. USDC at 4.11% and USDT at 4.64% are in line with what other Solana lenders pay on stables, sometimes a touch higher because lower TVL means a deposit moves utilization more. If you are lending stables, this is the number that matters.

Second, the LST pools look like they pay nothing, and that is a reporting artifact. jitoSOL and mSOL show 0.16% and 0.19% lending APY, but those tokens already carry roughly 6 to 8% staking yield in the token itself. You hold them as collateral, keep the staking yield, and the small lending base sits on top. The deposit is not the yield. The staking is. The marginfi LST token, by contrast, reports a 5.85% APY because that figure includes the staking component directly.

So the picture is not "MarginFi pays nothing." It is "MarginFi pays market rate on stables, and its biggest pools are LST collateral where the yield lives in the token, not the lending market."

The Security Picture

yieldwire scores the lending protocol at 71, Grade B, with HIGH confidence. That reflects the marginfi-v2 contracts, which have a multi-year track record, no recorded exploit, and audits from external firms that predate the rebrand. DeFiLlama lists zero audits in its registry, but that registry tracks formal submissions, not the full audit history. The contracts running today are battle-tested code.

The Project 0 wrapper is a different entry, and a more cautious one. yieldwire flags it as ungradeable, effectively a D, because the new prime-broker layer has no published audits under the Project 0 entity yet. The cross-margining ambition adds surface area that the older lending audits never covered.

The honest read: the lending you do today touches the proven marginfi-v2 markets, which is the B-grade part. The newer prime-broker functionality is unaudited under the new brand and should be treated as early. Size positions accordingly.

There is also a governance dimension. A rebrand plus a fresh token plus a new prime-broker thesis is a lot of change in a short window. Token launches reshape incentives. Watch how emissions and governance settle before assuming the rate environment is stable.

You can see the full breakdown on the MarginFi protocol page and the Project 0 page, and read how the grades are built on our security methodology.

Where It Fits

Context matters here. Kamino runs $2 to $3B in TVL and is the default lender on Solana. MarginFi at $29M is roughly two orders of magnitude smaller. That gap is the whole story.

Thin TVL cuts both ways. On the upside, your deposit moves utilization more, which can push your supply rate above the deeper venues, and the stablecoin numbers above show that. On the downside, thin liquidity means worse borrow availability, more rate volatility, and a smaller buffer if sentiment turns again. A protocol that has already seen one confidence run is more exposed to the next one.

For a stablecoin lender chasing the best rate, MarginFi is worth a line in the comparison. For size, depth, and the lowest-drama option, the larger venues still win. Run the numbers side by side on the yields page and size any position with the calculator.

Bottom Line

MarginFi did not die, but it did not bounce back either. The relaunch as Project 0 solved the two things that broke it, the missing token and the leadership vacuum, while the liquidity that made it matter in the first place mostly stayed gone.

The yields today are honest and modest. Stables pay 4 to 5%. LST pools pay through the token, not the market. The lending contracts are proven. The prime-broker layer on top is new and unaudited under the new name.

If you deposit, do it for the stablecoin rate and the LST collateral flexibility, with eyes open about the size of the protocol and the freshness of the rebrand. Check the live security scores before you commit.

Supply APY and TVL figures pulled from on-chain lending data and verified against DeFiLlama as of June 12, 2026. TVL history (peak $811M on April 1, 2024) sourced from DeFiLlama's marginfi-lending series. Security scores derived from yieldwire's scoring methodology. Audit count reflects DeFiLlama's tracked registry; protocols may carry additional unregistered audits. Yields float with utilization and change continuously. This is not financial advice.

Track all Solana yields in real time

Compare APYs across lending, LP, and liquid staking protocols on the YieldWire dashboard.

Open Dashboard →