Flash Trade FLP: Perpetual LP Yields on Solana

Flash Trade turns perps traders into your yield source. Its FLP vault pays LPs from trading fees, margin costs, and liquidations. Around 15% APY, but the risks are real. Here is what the data says.

Perps Traders Pay You

Most DeFi yield comes from lending or liquidity provision. Perpetual LP vaults flip the script: you become the counterparty to leveraged traders, and you earn when they pay fees, get liquidated, or hold positions overnight.

Flash Trade is a decentralized perpetual exchange on Solana built around this idea. Its Flash Liquidity Pool (FLP) is a multi-asset vault that serves as the other side of every trade on the platform. When a trader opens a 20x long on SOL, they are borrowing exposure from your pool. You earn from the fees they pay to do it.

The model is not new. GMX on Arbitrum popularized it. Jupiter Perpetual Exchange runs a similar setup on Solana with its JLP vault. But Flash Trade takes a slightly different approach to composition, fee splits, and asset exposure that is worth understanding if you are looking at perps LP yields.

How FLP Works

FLP is an index-style token representing fractional ownership of a basket of assets: USDC, SOL, BTC, and ETH. When you deposit any of these assets, you receive FLP tokens proportional to your share of the pool.

The pool serves three functions simultaneously:

1. Counterparty to traders. Every leveraged position on Flash Trade borrows exposure from the FLP pool. Long SOL? The pool lends you SOL exposure. Short BTC? The pool takes the other side. This means LPs have net exposure to trader PnL. When traders lose, the pool gains. When traders win, the pool pays out.

2. Fee collector. Every trade generates fees: opening fees, closing fees, margin borrowing costs, and swap fees. 70% of all collected fees flow back to FLP holders. The remaining 30% goes to the protocol and FAF stakers.

3. Liquidation beneficiary. When overleveraged positions get liquidated, the liquidation penalties flow into the pool. High-volatility periods tend to generate more liquidations, which means more yield for LPs.

FLP auto-compounds all fees and trading PnL every hour. You do not need to claim or restake. The yield rolls directly into the token price.

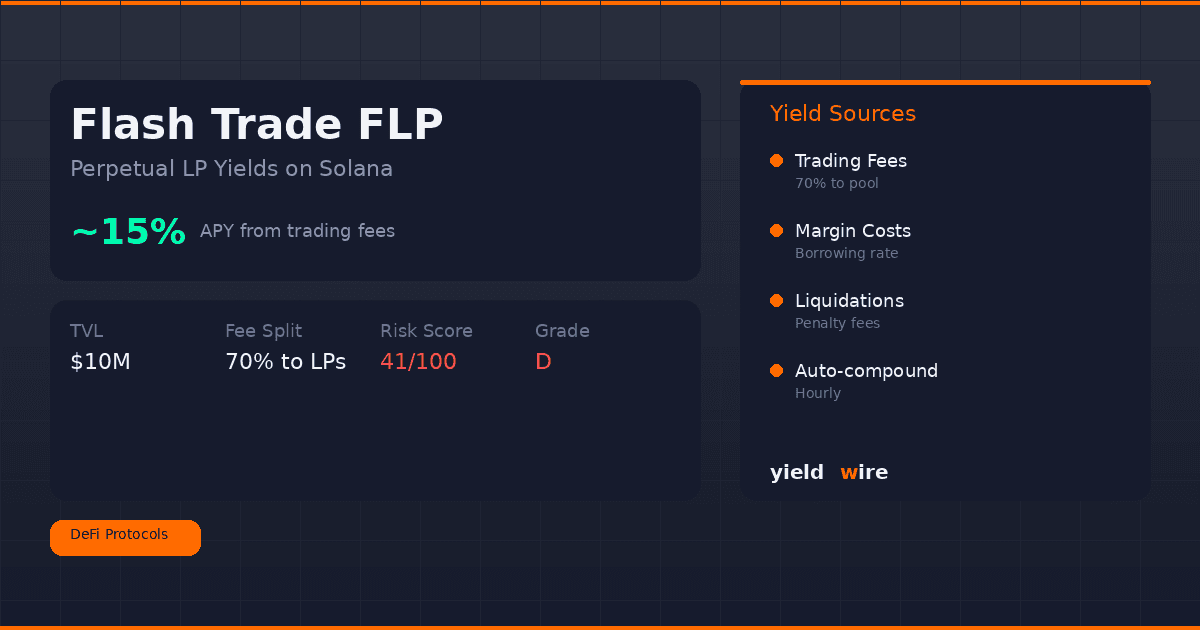

The Numbers

Here is what FLP looks like on yieldwire right now:

| Metric | Value |

|---|---|

| Current APY | ~15% (variable) |

| TVL | ~$10M |

| Yield source | Trading fees + margin costs + liquidations |

| Fee split to LPs | 70% |

| Auto-compound | Hourly |

| Assets in pool | USDC, SOL, BTC, ETH |

| yieldwire Risk Score | 41/100 (Grade D) |

That 15% APY is entirely base yield. No token incentives, no emission schedules. It comes from real trading activity on the platform. That is the good news.

The bad news is in the risk score. Let's unpack that.

Why the Risk Score Is Low

Flash Trade scores 41 out of 100 on yieldwire, placing it in Grade D territory. Here is why.

No public audits listed. DeFiLlama shows zero audits for Flash Trade. That does not necessarily mean the code has never been reviewed, but it means there is no publicly verifiable third-party audit that we can confirm. For a protocol holding user funds as counterparty to leveraged trades, this is a significant gap.

Relatively small TVL. At roughly $10M, Flash Trade's TVL is a fraction of Jupiter Perpetual Exchange ($691M) or even smaller lending protocols on Solana. Lower TVL means less battle-testing, thinner liquidity for large positions, and higher concentration risk for LPs.

Derivatives category risk. Perpetual exchanges carry inherent complexity: oracle dependencies, liquidation mechanics, funding rate calculations, position management. Each of these is a potential attack surface. The derivatives category on Solana averages a risk score of 50, and Flash Trade sits below that.

Counterparty exposure. Unlike lending, where your downside is limited to borrower defaults (usually overcollateralized), perps LP means your pool pays out when traders are net profitable. A sustained directional move where most traders are on the right side can draw down the pool. This is not theoretical. It happens during strong trends.

For the full methodology behind these scores, check how we score risk.

FLP vs JLP: The Solana Perps LP Comparison

Jupiter Perpetual Exchange runs the largest perps LP vault on Solana through its JLP token. The comparison is natural:

| Factor | Flash Trade FLP | Jupiter JLP |

|---|---|---|

| TVL | ~$10M | ~$691M |

| APY (approx.) | ~15% | ~8-12% |

| Fee split to LPs | 70% | ~75% |

| Assets | USDC, SOL, BTC, ETH | SOL, ETH, BTC, USDC, USDT |

| Risk Score | 41 (D) | 60 (C) |

| Audits | 0 listed | 0 listed* |

| Auto-compound | Hourly | Continuous |

*Jupiter's audit situation is nuanced. The main Jupiter exchange has been through extensive review, but the perpetual exchange component launched separately.

JLP has 69x more TVL, which means more liquidity, more trading volume feeding fees, and a larger pool to absorb trader wins. Flash Trade's higher APY partly reflects its smaller size: the same dollar of fees distributed across less capital produces a higher percentage return.

This is a common pattern in DeFi. Smaller pools often show higher APY. The question is whether that higher APY compensates for the additional risk of a less-tested, less-liquid protocol.

Who FLP Is For

FLP makes sense for a specific type of DeFi participant:

You want real yield, not token farming. FLP's returns come from trading activity, not emissions. If the protocol has volume, you earn. If it does not, you do not. There is no governance token propping up the number.

You understand counterparty risk. Perps LP is fundamentally different from lending or staking. You are taking the other side of leveraged trades. In most market conditions, traders as a group lose money (the "house edge"). But in strong trends, the pool can take temporary drawdowns.

You are comfortable with the risk profile. Grade D on yieldwire means below-average security posture. No audits, low TVL, derivatives complexity. If you are allocating here, it should be with capital you can afford to lose, and it should be a small portion of your overall DeFi position.

Ecosystem Integration: Xitadel LTT

One recent development worth noting: Xitadel launched a Liquid Treasury Token (LTT) using staked FLP (sFLP) as collateral. This 90-day instrument offered a fixed-rate return backed by the yield that FLP generates. It is an early example of composability around perps LP tokens, where the yield from being a trading counterparty gets packaged into a structured product.

This kind of integration tends to grow TVL over time, as it gives FLP holders additional options beyond simply holding.

The Bottom Line

Flash Trade FLP offers one of the highest base yields on Solana at around 15%. It is real yield from real trading activity, not inflated by token incentives. The 70/30 fee split is competitive, and hourly auto-compounding removes the friction of manual claiming.

But the risk profile is real. No public audits, $10M TVL, derivatives complexity, and direct counterparty exposure to leveraged traders. Our risk score of 41/100 reflects these concerns.

If you are exploring perps LP yields on Solana, compare FLP against JLP on yieldwire before making a decision. The data is there: APY, TVL, risk scores, and fee structures, all side by side.

Compare perps LP yields on yieldwire →

yieldwire tracks 130+ Solana protocols and 3,500+ pools with risk scoring across 6 factors. None of this is financial advice. Do your own research.

Track all Solana yields in real time

Compare APYs across lending, LP, and liquid staking protocols on the YieldWire dashboard.

Open Dashboard →